Bad Debts Written Off Journal Entry

The recovery of a bad debt like the write-off of a bad debt affects only balance sheet accounts. Debit Credit Accounting Quiz.

Bad Debt Write Off Journal Entry Double Entry Bookkeeping

Otherwise a business will carry an inordinately high accounts receivable balance.

. Journal Entry for Recovery of Bad Debts. 03 December 2008 It means that you are writing off clearing or deleting irrecoverable debtors from your books. Not all debtors pay their dues every time.

Is a manufacturing concern with two stitching units. In the journal entry it debits bad debt expenses while crediting the amount it expects to be paid. See also Accounting for Written Off Bad Debts.

Bad debts written off - general journal or bad debts account. So the firm does not want to write off the sum for the time being. Microfinance services are designed to reach.

Read more is recorded as a direct loss from defaulters writing off their. Bad debt is usually a product of the debtor going into bankruptcy but may also occur when the creditors cost of. And payment systems among other services.

Here is an example of a depreciation journal entry. If instead the allowance for uncollectible accounts began with a balance of 10000 in June we would make the following adjusting entry instead. Bad debts provision Bad Debts Provision A bad debt provision refers to the reserve made by a company to set aside an amount computed as a specific percentage of overall doubtful or bad debts that has to be written off in the next year.

This implies that some of the credit customers might not pay their debts in time. This shows investors how much receivables are still good. In the next financial year the debt becomes bad debt which needs to be written off.

Maybe more importantly it shows investors and creditors what percentage of receivables the company is writing off. 2 Next the Company needs to initiate the following entry to write off the bad debt of customer A. Partially or fully irrecoverable debts are called bad debts.

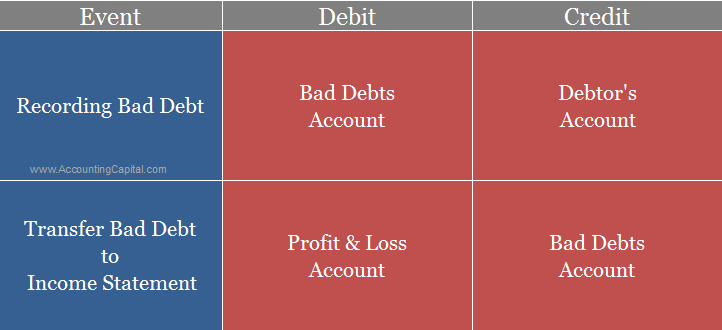

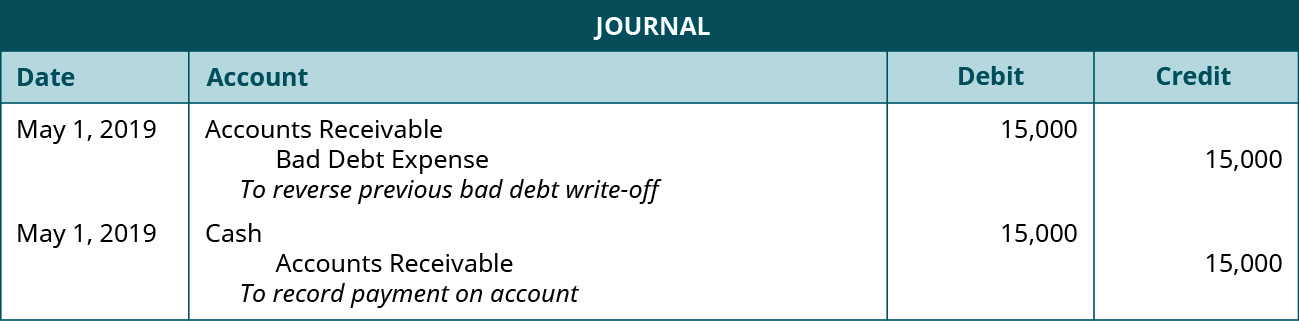

Savings and checking accounts. Notice that this entry is exactly the reverse of the entry that is made when an account receivable is written off. Accounting and journal entry for recording bad debts involves two accounts Bad Debts Account Debtors Account Debtors Name.

However the customers sometimes pay the amount written off as bad debts. The following journal entry is made for this purpose. When a customer pays after the account has been written off two entries are required.

Trading Profit and Loss Account. Microfinance includes microcredit the provision of small loans to poor clients. When a written of account is recovered the first step is to reinstate it in the accounting record.

Microfinance is a category of financial services targeting individuals and small businesses who lack access to conventional banking and related services. Enter the name of the person you made the loan to and the phrase bad debt statement attached in column 1 of Part 1 line 1. The expenses may include the appraisal fees registration charges accounting fees regulator charges loan marketing expenses regulator fees and all other related.

In this case the journal entry to record the bad debt expense would be. While posting the journal entry for recovery of bad debts it is important to note that it is treated as a gain to the business that the debtor should not be credited as in. 80000 and it is doubtful that the customer may not pay the sum.

Accounting Treatment for Asset Disposal. Above we assumed that the allowance for doubtful accounts began with a balance of zero. Try Another Double Entry Bookkeeping Quiz.

The billing to the customers. The Bad Debts Expense remains at 10000. It would be double counting for Gem to record both an anticipated estimate of a credit loss and the actual credit loss.

The journal entry above shows that the treatment required to reduce accounts receivables as well as record the written-off accounts as an expense in the financial statement. For companies that sell goods and services on credit bad debts are a common occurrence. Bad Debts Written Off Income Statement 2000.

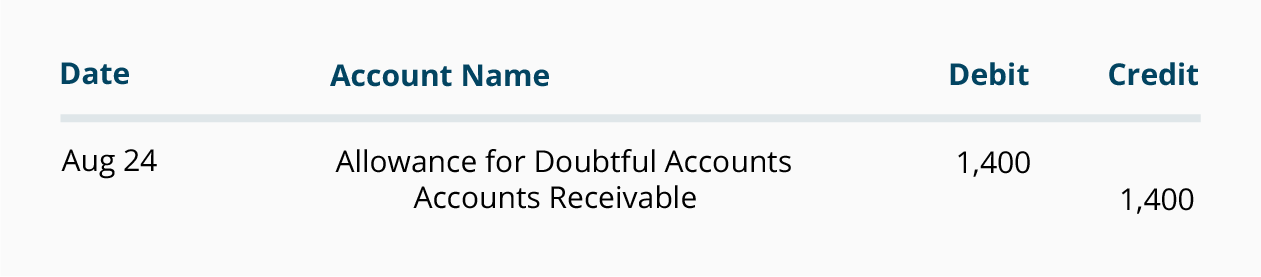

However we need to understand that bad debt write off is not consistent with the Matching concept. Suppose the amount due from a customer is Rs. When a doubtful debt turns into bad debt businesses credit their account receivable and debit the allowance for doubtful accounts.

Accounting and journal entry for recording bad debts involves two accounts Bad Debts Account Debtors Account Debtors Name. Irrecoverable debts are also referred to as bad debts and an adjustment to two figures is needed. At times a debtor whose account had earlier been written off by a creditor as a bad debt may decide to make a payment this is called the recovery of bad debts.

Bad Debts Written Off. The concept of Asset Disposal is illustrated in the following example. The accounts receivable test is one of many of our online quizzes which can be used to test your knowledge of double entry bookkeeping discover another at the links below.

Below are the examples of provisions for a bad debt journal entry. 70000 written-off as a bad debt being transferred to bad debts. The first approach tends to delay recognition of the bad debt expenseIt is necessary to write off a bad debt when the related customer invoice is considered to be uncollectible.

If you never. Explanation of Provision for Bad Debts. Irrecoverable debts Writing off an irrecoverable debt means taking a customers balance in the receivables ledger and transferring it to the statement of profit or loss as an expense because the balance has proved irrecoverable.

It is not directly affected by the journal entry write-off. A bad debt provision is a reserve made to show the estimated percentage of the total bad and doubtful debts that need to be written off in the next year. See uncollectible accounts expense allowance method.

1 The entry made in writing off the account is reversed to reinstate the customers account 2 The collection is journalized in the usual manner. Instead it is reported at its full amount with an allowance for bad debts listed below it. The bad debts expense recorded on June 30 and July 31 had anticipated a credit loss such as this.

Journal Entry for Bad Debts. 1 Direct Write-Off Method. Set off or contra entries- general journal.

Bad debt is debt that is not collectible and therefore worthless to the creditor. The debit to bad debts expense would report credit losses of 50000 on the companys June income statement. For example X is your debtor from last 2 years for Rs.

Hence these assets need to be written off from the Balance Sheet since they no longer fulfill the asset recognition criteria laid out by assets. It is simply a loss because it is charged to the profit loss account of the company in the name of provision. Definition Example and Journal Entries Sometimes the business has to bear significant expenses in the process to raise the finance.

A bad debt can be written off using either the direct write off method or the provision method. Trade Debtor Accounts Balance Sheet 2000.

What Is The Journal Entry For Bad Debts Accounting Capital

3 3 Bad Debt Expense And The Allowance For Doubtful Accounts Financial And Managerial Accounting

Writing Off An Account Under The Allowance Method Accountingcoach

Write Off Bad Debts Manager

No comments for "Bad Debts Written Off Journal Entry"

Post a Comment